Table of Contents

Introducing statement of owner’s equity

The report of owner’s equity shows the general changes in the account of the prime capital. Besides, these changes happen due to net income or loss, contributions, and withdrawals of money. The income and aid of the owner increase the capital of the business. Besides, the costs and the withdrawals of cash drop the amount of the total wealth. However, this report is for sole ownership business. It shows statement of owner’s equity the flow in the capital.

The other name of the equity statement is the report of changes in equity. But, it is a financial report and crucial for any company or business governing body. Besides, equity is a simple term. It is the primary money that the owners invest in their business. It includes all the added earnings. A company needs to prepare a report on the owner’s equity at the last of every fiscal year. Besides, they may make it with other business documents. It reports on the changes in the equity of the business. But, it deals with the starting and the ending balance within a fixed period.

Also, the time is one fiscal year. The change of the equity includes some basic terms. They are the earned income, payments, inflow and outflow of the equity, net profit, net loss, etc.

What is equity

Equity is a simple term. It means the money that the shareholders invest in a business. Besides, it sets up partial capital from the total investment in the industry. This part does not go to the debt owners. Moreover, there is a place or a section for the shareholders’ equity on the business’s balance sheet. This section has three sectors. They are,

- Net Income

- Share Capital

- Retained earnings

What is owner’s equity?

Generally, the owner’s equity is his rights to the main assets of the company. Firstly, subtract the primary support charges, and you will get some properties for the company’s owner. This amount is his equity.

After that, look at the balance sheet of your company. You will find that it follows a simple accounting equation. The equation is as follows,

The owner’s equity = Assets – Liabilities

Besides, equity of the owner is a vital term for single ownership.

What does owner’s equity include?

The owner’s parity may include the followings,

- The invested money or asset of the owner of the company.

- Extra profits of the business.

- Reduced profits of the business since the owner take it out.

- Minus asset because of debt.

If the business gets a structure of a firm, the equity may have some accounts like the followings,

- Reserved earnings.

- Common stock

- Treasury store

- Ideal stock

- Addition paid-in basic

The owner’s equity is not an asset on the balance sheet?

The owners of the company may think that the equity of the owner is an asset. But, it is not an asset according to the balance report of the business. Generally, The equity of the owner is the property of the company’s owner. But, the company is not the owner itself. The equity of the owner is one kind of liability to the company. Besides, it denotes whatever the owner claims. Moreover, it signifies the leftover asset’s claims if the company sells its properties and pays its debt.

Can the owner’s equity be negative?

There will be many questions on the equity statement. Mostly, the readers may ask if the owner’s equity can be minus or not. The answer is yes. It happens when the liabilities of a business become higher than its assets. In that case, the investors have to invest more money in the company. Thus, they can cover the shortage of funds.

Generally, the company faces this situation. Then, the owners take the investment back from the company. This amount can be taxable. You can consider it as the capital additions on the tax return. That’s why the company owners have to see the capital balance sheet regularly. Besides, they should not take the money back from the business. They should try to make the capital positive again. Withdrawal of total cash from the asset is a bad thing for business.

How to calculate owner’s equity

Suppose you want to calculate the owner’s equity of a company. Firstly, add up all of the assets of the company. After that, deduct the liabilities from the deal.

For example, consider a fictitious company, Rodney’s Restaurant supply. It is the starting year of their business. They had the following transactions,

- Firstly, They have invested about $25,000 in renting a place. Besides, they also have used this money to pay the startup expenses and to buy primary inventory.

- However, the company got extra funding from a loan.

- The company had a net income of $170,000 in the first year. The income report has shown this. However, they calculated it considering all expenses and revenues.

- The owner, Mr. Rodney, withdrew about $70,000 from his business.

What is a statement of owner’s equity?

The statement of owner’s equity is a short economic report. Besides, it does not contain a lot of transactions. However, they do not affect the equity accounts a lot. It only lists down the net income or the net loss. Besides, it also considers the withdrawals and contributions of the owners during a specific . This report consists of some points.

- Starting equity balance

- Net income

- Owner’s aid

- Net loss

- Owner’s withdrawal

- Final equity balance

The statement of owner’s equity gives some details. Such as:

- The initial balance of the proprietor’s prime account

- Growths of equity from incomes or extra capital aids

- Reduction to equity from the capital shares or losses

- The final amount of the holder’s capital account

The final balance on the report of the proprietor’s equity should be equal to the equity accounts. However, it will take place at the company’s balance slip for the fixed fiscal period.

Purpose and importance of the statement of owner’s equity

Generally, you mention the owner’s equity in the balance slip. Sometimes, it is hard to learn the leading cause of changing the owner’s financial records. Generally, it happens for the more prominent firms. This record helps the users to find out some factors. Besides, these factors change the owners’ parity over the fixed period. The deviations’ statement in the equity discloses essential evidence about equality. Also, you cannot present it alone except in the fiscal record. This record is crucial for outer users. They can realize the character of changes in the equality accounts.

Line items of the statement of owner’s equity

There are some line objects of the equity record. There are as follows,

Opening Balance

However, a new year’s starting balance is the final balance of the previous year’s report of owner’s equity. Also, there will be more addition and subtraction at this balance in the current fiscal year. All of these will help to make the equity report balance.

Net Income

A firm earns an amount of money in a financial year. Besides, this fixed amount of money of every fiscal period is the net income of that company. But, the company considers this income after subtracting all other working and non-operating costs. Besides, the firm takes the value from the income report. Another name of this report is the gain and loss statement. The finance section of the company prepares this report at the end.

Other Incomes

Also, there will have some extra earning for the company. This income, for example, some unrealized or actuarial gains from fiscal instruments. The income report maybe will not recognize this income.

Matter of New Capital

At an exact time, there will be an issue of new shares. Besides, there will be an arrival of new capital or a new addition to the owner’s equity of the company. The owner adds it to the total equity.

Net Loss

A company may suffer some losses due to its operation through a fiscal year. However, it is a common thing in any business. This kind of cost is the net loss of the company. Besides, it decreases the total capital of the industry. The equity report shows it as a deduction.

Other losses

A company or business may have different kinds of earnings, as well as losses. There are some losses or expenses that a company may face. These losses are crucial for the company. But, the fiscal report does not spot these vast losses. Besides, they may cause budgetary derivatives.

Dividends

The dividend is one kind of reward. It is the return income by the owners of a company. But, they invest money for the business and get a payment in return. This fee reduces the total equity of the investor that they won at the company. Also, it deducts from the equity report of the owner.

Extraction of the Capital

Sometimes, the company withdraws its money from their deal. As a result, they redeem their shares of the business. The owner’s equity statement displays it as an inference of the asset because it reduces its total parity.

Elements of the financial statement of owner’s equity

The financial report has some vital parts. They are as follows,

Assets

The assets are the items or the company’s money. Besides, the owner of the company tries to claim it.

Investment by owners

Some investors invest some cash or other products or assets in the company. Besides, they invest in exchange for the title of the business.

Revenue

Revenue is the value of facilities and goods the company already has given or sold.

Expenses

Expenses denote the costs by the group to provide the things or facilities. Besides, the company earns the profits from them.

Gains

The gains are the same as the revenue. But, they have a relation to the minor actions of the business.

Losses

The losses have similarities to costs. But, they are related to the outer deeds of the company.

Liabilities

The liability has another name, creditors. Liability is the amount of money that the company is in debt to others.

Equity

Equity is the net assets or the net value of the business. Besides, it is the critical point of the statement of owner’s equity.

Complete income

Total income is the general change in the equity of a company. But, this change happens during a fixed time. It starts from the trades at the start of the fiscal year.

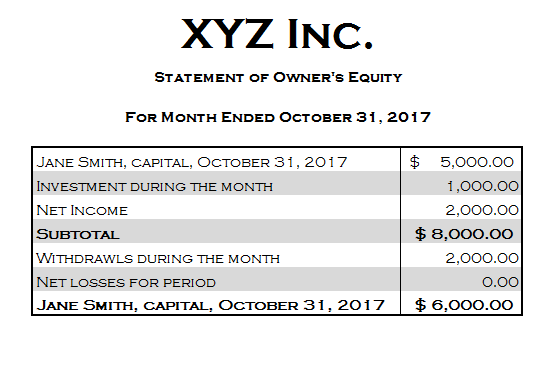

Wrapping up with the statement of owner’s equity or SOE

The report of owner’s equity presents the prime capital of the owner. But, it shows the money at the start of the year. This equity changes and affects the capital. Besides, it also affects the resulting wealth in the end. So, its other name is the report of changes in owner’s equity. The usual SOE has a heading that consists of three outlines. Firstly, the starting line represents the company’s name. After that, the second line shows the label of the statement. Finally, the last line denotes the covered period.

The amount of capital varies from business to business. But, income increases the worth of a company. On the other hand, capital sees a fall in costs. You can get the net income by subtracting expenses from the earning. But, the net income may grow the total wealth. When the total costs exceed the total revenue, you may experience a net loss. So, the net loss may drop the capital money.

Generally, the success of a business depends on the year-to-year increment of an owner’s equity. But, the company should monitor it often. Thus they can make more profit.