The operating cash flow formula is a skill count method that helped measure the cash of a business. However, a business that makes cash from its core activities and business activities deduct operating expenses from total income. Firstly, it determines how much cash creates from the business operations. It does not consider petty sources of revenue like interest or investments.

In theory, cash flow calculation isn’t complex. It’s a symbol of how money transfers into and out of your business. But for the most vital numbers of small business owners, the simplicity ends there. Fixing a cash flow formula is separate from accounting for profit or gains alone. However, there’s a lot more to it, and that’s wherever many heads get lost in the weeds.

But for all of the small businesses, in particular, this cash flow is also. However, it is one of the highest essential parts that provide your business’s financial health. Once, one study told that around 30% of businesses fail because the owner goes out of money. And 60% of tiny business owners don’t feel conscious about accounting or finance. Above all, when notes come due, you have to cash to pay them.

Table of Contents

What is the Operating Cash Flow Formula

The Operating Cash Flow Formula is a robust computing method. Also, it helps to calculate a company’s cash inflow and outflow from its operating activities. By this, the investors and creditors can see what the condition of a company’s operations is. However, it also results in a company’s ability to expend money for its primary activities. This theory is essential for financial guesses since it can help to show the health of a company. However, all private and public companies should report their quarterly financial reports and annual cash statements. It is better to use the indirect method to compute this value.

Types of Cash Flow from Operating Activities

The cash flow from the operating activities is generally two types. They are:

- Indirect method

- Direct method and

Indirect Method

The first method is the indirect method, where the company works with a net profit on a growth accounting base. And also serves backward to gain a cash basis figure for the time. Below the growth system, revenue confesses when it earns, not indeed when cash will take. Therefore, net income magnifies this amount on a cash basis.

For example, if a client purchases a $500 widget on credit. The sale had formed, but the cash had not still been accepted. The company yet recognizes the income in the month of the sale. And displays up in net income on its income statement.

Therefore, net income is amplified by this amount on a cash basis. The offset to the $500 of income would seem in the accounts receivable list part on the balance sheet. There needs to be a decrease from net profit in the $500 rise to accounts receivable due to this sale on the cash flow statement. It can show on this statement as “Increase in Accounts Receivable -$500.”

Direct Method

Another method is the direct method, in which all transactions of a company lists on a cash basis. And presents the data on the cash statement utilizing actual cash inflows and outflows throughout the accounting period.

The elements of the direct method of cash flow from the operating system:

- Salaries paid out to employees.

- Cash paid to merchants and suppliers.

- Cash received from clients.

- Investment income and profits received.

- Income tax paid and interest paid.

The Transparency of Operating Cash Flow Formula

Operating cash flow is a clear symbol of whether a business is truly profitable. And for that reason, the investors and creditors often want to know this number. One of the most significant points of a successful business is that it makes more money than it takes to produce a product. Yet other expenses and earnings can shrink these numbers depending on how the business owner chooses to present. Operating cash,

however, is very natural, highlighting potential problem areas of the business.

For example, let us say that a business is losing the meaning of such retail activities in one aspect of its business. But it is still making money on outside treaties or investments. Looking at the overall cash flow, this company may seem profitable. However, further exploration of income sources makes it clear that this business’s core is not sustainable. These insights are just as valuable for potential investors as they are to business owners. This shows the severe need to switch the business model of a company.

Cash Flow Formula

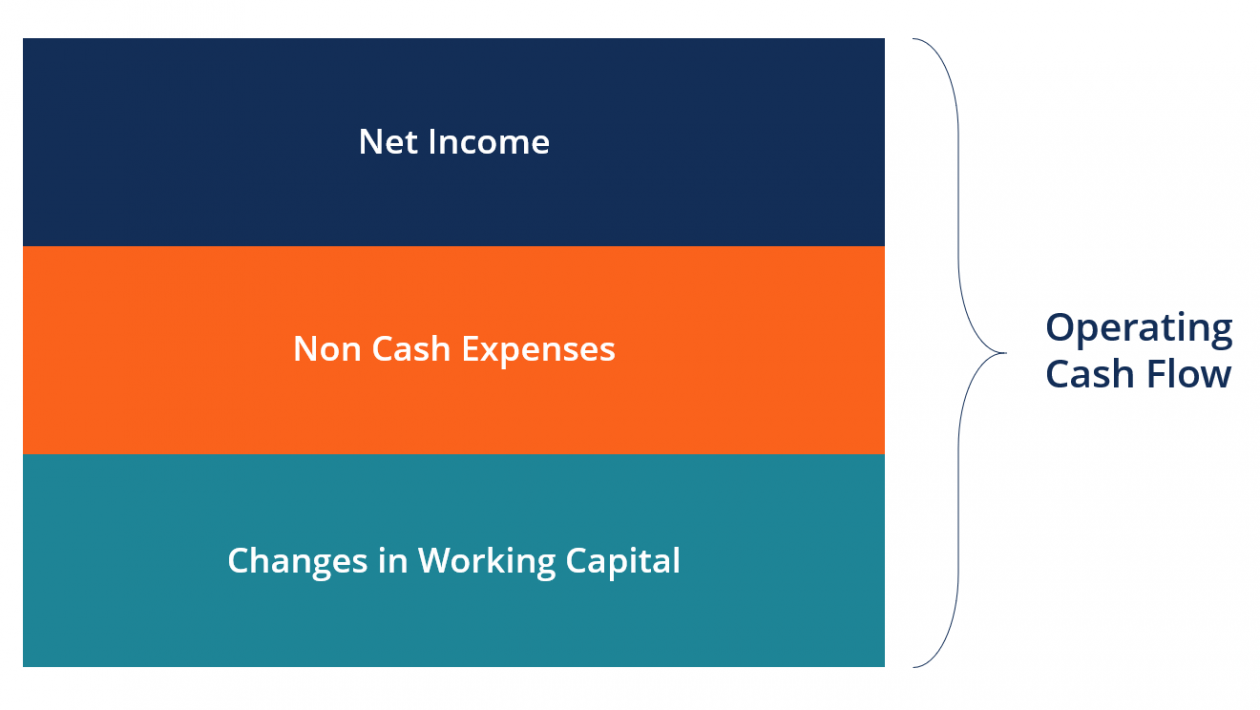

- Operating Cash Flow Formula = Operating Income + Depreciation – Taxes + Change in Working Capital.

- Free Cash Flow Formula= Net income + Depreciation – Change in Working Capital – Capital Expenditure

- Cash Flow Forecast = Beginning Cash + Projected Inflows – Projected Outflows = Ending cash

Operating cash flow formula

One of the most common and vital cash formulas is the operating cash flow formula.

While a standard cash inflow and outflow report gives you a view of your business’ cash at a given time, that doesn’t constantly help you with planning and budgeting because it doesn’t consider the cash you have available or free to use.

Can you manage to fund for new software? Do you have well cash on hand to spend for that pragmatic assistant when their invoice comes due?

Calculating the operating cash flow helps answer those questions and others like them.

How to calculate operating cash flow

Calculating your institution’s operating cash inflow and outflow is simpler than you might think. Firstly, you’ll require accounting software to create your institution’s income statement. And you need to know the balance sheet ready to pull key economic numbers from.

First, let’s get the appropriate financial terms straight.

The basic operating cash flow formula is

Operating Cash Flow = Operating Income + Depreciation – Taxes + Change in Working Capital.

To apply the operating cash formula to our prior model, let’s say financials for the year look like this:

Operating Income = $85,000

Depreciation = $0

Taxes = $9,000

Change in Working Capital = – $10,000

The operating cash formula is represented by:

[$85,000] + [$0] – [$9,000] + [-$10,000] = $66,000

That means, in a normal year, it produces $66,000 in actual cash from typical operating activities.

Free cash flow formula

One of the most evident and significant cash formulas is the free cash flow formula.

While a standard cash report gives you a view of your business’ cash at a given time, that doesn’t constantly help you with planning and budgeting because it doesn’t absolutely consider the cash you have available or free to use.

How to calculate free cash flow

Calculating your institution’s free cash inflow and outflow is simpler than you might think. Firstly, you’ll require accounting software to create your institution’s income statement. And you need to know the balance sheet ready to pull key economic numbers from.

First, let’s get the appropriate financial terms straight.

Free Cash Flow = Net income + Depreciation – Change in Working Capital – Capital Expenditure.

Let’s discuss an example of that formula in the real world. Suppose Rakib is a freelance graphic designer. He needs to determine his free cash to see if utilizing a virtual assistant to manage client admin jobs is financially feasible.

His financials for the year look like this:

Net income = $80,000

Depreciation = $0

Change in Working Capital = – $10,000

Capital Expenditure = $2,500

[$80,000] + [$0] – [$10,000] – [$2,500] = $67,500

That means he has $67,500 in ready cash to reinvest back into his institution.

Cash Flow Forecast formula

While free cash inflow and outflow provide you a good conception of the cash available to reinvest in the business, it doesn’t always give the perfect view of your routine, everyday cash statement. That’s because this formula doesn’t estimate irregular spending, gaining, or investments. If you sell off a fixed asset, your free cash will go way up. But that doesn’t match the regular cash statement for your institution.

When you require a better idea of typical cash for your institution, you want to use the Cash Forecast formula.

Cash obstacles are never fun, so it’s essential to ensure accurate cash before you start consuming.

How to calculate your cash flow forecast

Calculating your institution’s forecast cash flow is really simpler than you might think. There are not any that exist for complex financial terms. It’s just a simple computation of the cash you require to bring in and spend during the next 30 or 90 days.

The formula looks like this.

Cash Flow Forecast = Beginning Cash + Projected Inflows – Projected Outflows = Ending cash

Beginning cash means how much cash your business has on hand today. And you can pull that amount right off your Statement of Cash. Scheme inflows are the cash you demand to gain through the given period. That involves current statements that will come due and future invoices for which you demand to send and receive payment. Project outflows are the costs and other payments you’ll make in the given timeframe.

Getting back to our Rakib’s example, let’s say he has:

Beginning cash = $30,000

Projected inflows for the next 90 days = $30,000

Project outflows for the next 90 days = $4,000

Here’s what her cash flow forecast looks like:

[$30,000] + [$30,000] – [$4,000] = $56,000

That means he has $56,000 ready to cash to reinvest back into his institution.

Operating Cash Flow Calculator

You can use the operating cash calculator to instantly determine the operating cash inflow and outflow by entering the expected numbers.

Net Income

100

Noncash Expenses

25

Increase in Working Capital

25

Operating Cash Flow (OCF)

$100.00

Key takeaways

- The operating cash flow formula is an important benchmark to conclude the financial progress of an institution’s core business activities.

- Cash from operating activities is the first division depicted on a cash statement. Which also involves cash from investment and financing activities?

- However, are two methods for representing cash from operating activities on a cash statement report? They are the indirect method and the direct method.

- However, the indirect method starts with net income from the income statement. Which adds back noncash items to appear at a cash basis figure?

- And, the direct method follows all transactions in a season on a cash basis. And uses genuine cash inflows and outflows on the cash report.

Operating Cash Flow Conclusion

- Firstly, the operating cash flow formula estimates the amount of cash produced by a company’s average trading operations.

- Then the formula for operating cash needs three variables. They are net revenue, noncash costs, and an extension in working capital.

- However, operating cash is a significant number to estimate the economic success of an institution’s core business activities.

- And, operating cash is the first part of a cash statement.

- There is a short and long variant of the method for determining operating cash.

- Finally, there are two various methods for depicting determining cash statements. They are the indirect method and the direct method.

Conclusive Discussion

Above all, we can hope that now you can know all about the operating cash flow formula. We tried and researched a lot to explain the whole thing in a simple and easy way. If you have any questions, then feel free to knock us by the comment box. We will try to appreciate your queries.